Eneti Stock: Weak Q4 Earnings and Conference Call (NYSE: NETI)

Charlie Chesvick/E+ via Getty Images

Shares of wind turbine installation vessel (“WTIV”) owner Eneti (NETI) are down more than 50% since I launched coverage of the company 14 months ago.

At that time, the company was still operating as “Scorpio Bulkers” and was in the process of selling off its entire fleet of dry bulk carriers just before the Baltic Dry Bulk Index (“BDI”) rallied to new multi-year highs after languishing for more than a decade.

It wasn’t actually the first time management had exhibited exceptionally bad timing. In 2019, the private arm of the Scorpio Group, Scorpio Services Holding, acquired the struggling offshore service vessel provider Nordic American Offshore, which was later renamed Hermitage Offshore Services to be liquidated in bankruptcy a few quarters later.

At the end of 2020, I hoped that market players would discover the company as the next hot ESG game after the highly anticipated announcement of his first new build WTIV order, but things didn’t go as planned by me.

At the beginning of August, the company surprisingly announcement the acquisition of Seajacks International Limited (“Seajacks”)”become the world’s first owner and operator of wind turbine installation vessels“.

The transaction not only significantly diluted Eneti’s existing shareholders while triggering $30 million in executive bonuses, but also significantly weakened the company’s balance sheet.

With most of the company’s cash having been devoted to the acquisition of Seajacks, a number of alleged short and medium term debt maturities and the stated intention of management to exercise the option to build a second new WTIV at a cost of $326 million, Eneti apparently recognized the need to raise additional capital.

The announcement clearly caught market participants off guard as it took several days for underwriters to align investors, but the deal with gross proceeds of $175 million was still deep in the hole and in fact did not. managed to raise the targeted amount of $200 million despite insiders. and related parties buying more than 20% of the new shares.

In recent weeks, Eneti has managed to do extra work for its WTIV fleet, received commitments for a new $175 million credit facility and repaid a total of $105.3 million in debt related to the Seajacks.

Additionally, the company has decided not to move forward with plans to build a Jones Act-compliant vessel due to the perceived likelihood that international WTIVs will be required to meet high market demand. US scheduled for 2024 and beyond.

On Thursday, Eneti announced weaker-than-expected fourth-quarter results, mainly due to late customer payments and high operating expenses.

Following the earnings release, management staged a disastrous conference call that left a number of analysts scratching their heads, as evidenced by a number of tough questions during the Q&A; session.

Perhaps the most embarrassing part of the call was CEO Emanuele Lauro’s apparent lack of expertise (emphasis added by author):

Benjamin Nolan

(…) And then, James, I was going to come back to the G&A; side. I think you were talking about $7-8 million in cash G&A.; When I kind of look at what’s normal for the rest of the industry, most other companies, their full G&A; on a quarterly basis is $3 million, maybe $3.5 million. So it’s a bit higher. Is — what — can you explain to me what the difference is, like why yours might be higher?

Emmanuel Lauro

I think — that’s Emanuele here. I think it’s hard to say why or compare, as I don’t know of any other companies. So we are only telling you what we ourselves are. I can’t afford to compare myself to other companies operating in the same space. As we discussed, we just opened. This is the first quarter we announced as a fully integrated business after the merger with Seajacks, so there may be changes in the future, but that’s what it is today. So we guide you to where we are.

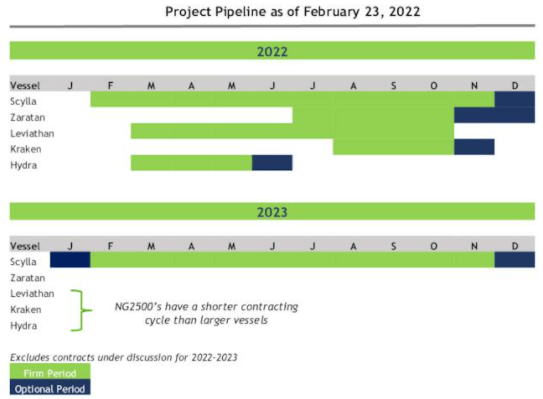

Additionally, the company announced a three-month delay in the start of the planned contract for the high-spec WTIV.”Zaratanwhich is now expected to remain inactive for the first half of the year.

Company presentation

With the flagship of the company “Scylla“already booked for most of 2022 and 2023, the company will likely face challenges securing significant additional work for its smaller vessels”Leviathan“, “kraken” and “Hydra“.

For 2023, management was hopeful for the Zaratan find a job off Taiwan.

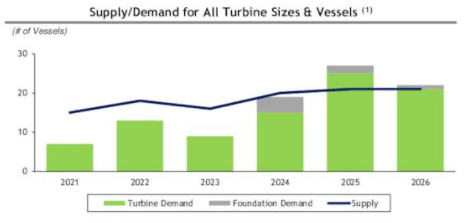

Recall that the WTIV market continues to suffer from an oversupply of vessels with a real inflection point expected before 2024:

Company presentation

The company also forecast direct vessel operating expenses to remain at high levels as COVID-related restrictions resulted in the requirement to operate three crews instead of two, with most crew residing in Europe while the “Scylla“is currently working in Asia. As a result, operating expenses for the company’s high specification vessels are currently more than 40% higher than pre-COVID-19 levels.

Finally, management backtracked on previous expectations to announce a first contract for its first new WTIV this summer.

Pro forma for the new $175 million term loan facility and recent $87.7 million debt repayment, Eneti’s current cash is $241.3 million, sufficient to cover expected operating losses and scheduled payments for its two new build WTIVs through to the lump sum payment of $198.2 million for the first vessel. will be due in Q3/2024.

Assuming Eneti manages to arrange financing at the usual rate of 60% loan-to-contract ratio, the company should be able to take delivery of the two new builds without raising additional capital.

Conclusion

Eneti stock took a well-deserved beating on Thursday after announcing weaker-than-expected fourth-quarter results and management’s embarrassing performance on the conference call.

Although the stocks are trading at favorable levels, I find it increasingly difficult to recommend the stock given the weak near-term industry outlook, high operating levels and major management issues. .

That said, results should improve significantly in Q3 as both high-spec WTIVs will be under contract for the entire quarter. Going forward, potential catalysts include:

- a major contract award in 2023 for the high specification WTIV”Zaratan”

- Eneti organizes the financing of the first new WTIV whose delivery is currently scheduled for the end of 2024

- major contract awards for the company’s lower spec fleet

- first potential contract for the first new WTIV

Given the issues discussed above, only the most speculative investors should consider an investment in Eneti at this stage.